| ||||||||||

|

Back when I was in high school, almost every Saturday, I'd take the bus and subway from my home in Malverne, Long Island into New York City to forage around the shops on Cortlandt Street for military surplus bargains. By experimenting and trying to get stuff working again, I learned a great deal about radios and electronics. In fact, I learned enough to set up a little after-school business repairing car radios which, in those days, were notoriously unreliable. By the time I was 15 (1954), I had saved a few hundred dollars from the business which, in those days, was a princely sum to a 15-year-old. I dearly wanted to buy an oscilloscope but Herb Bushman, a friend of our family, suggested that maybe I should buy a couple of shares of stock. Well, this was a fairly radical idea. My father had all of his meager savings in the bank and in some War Bonds and the only thing he knew about the stock market was that it caused a lot of investors to wind up in the poorhouse during the depression. It just so happened that right around then I had entered a contest sponsored by RCA in which you had to write in 75 words or less why you like RCA service instruments. Lo and behold, I won one of the 5th place prizes, a spanking new vacuum tube voltmeter, that was a whole lot better than the military surplus meter I was using. As a result, I put off the purchase of the oscilloscope and bought some shares of stock. I remember clearly that Herb was very emphatic about not just buying shares of one company, but buying three or four.  To this day, I remember clearly what I bought with the first $500: 2 shares of CBS (because I used CBS Hytron tubes in my business and because CBS had the most popular shows on television, Ed Sullivan and I Love Lucy). I also bought 2 shares of Standard Oil Co of NJ (for $61/share because we used Esso gas), 2 shares of Eastman Kodak, and 5 shares of American Sugar Refining. From these first small steps in investing, I learned four important lessons. Lesson 1: Diversify. Buying just a few shares of four stocks cost more in commissions than had I put all my money in one stock. But had I bought just one, it might well have been the wrong one. As it turned out, five years later, one of those stocks had gained just 9% while another one had nearly doubled. Lesson 2: Start investing early. Compounding is your best friend. The longer you have your money working for you, the more you will gain. During seven long years in college (BS, MS, MBA), I worked part time and summers and much of my income went toward college and automobile expenses. Nevertheless, I was able to add $500-600 to my investments each year during college and my two years in the Army. Thus, when I got out of the Army in July 1965, I was able to make a down payment on a house in a nice section of Pittsburgh and still have a stock portfolio worth more than $10,000.

With a few additional stocks, the holdings in my portfolio in 1968 were pretty much the same as they were ten years earlier. This was beginning of the go-go years of conglomerate companies like Gulf & Western, Walter Kidde, and Textron. I signed on with a new stock broker who felt that I was hopelessly out of touch with the market and came up with an aggressive plan to redo my portfolio for the 70's. So I did a lot of buying and selling just before the horrible bear market on 1969-70. I watched the value of my new, wonderful portfolio sink by nearly 50%, changed jobs (nothing to do with the stock market), and moved to the Boston area. Again, I signed on with a new stock broker who again had totally different ideas about the movers and shakers of the market, so by the end of 1972 only one of the companies that I held four years earlier was still in my portfolio. The good news was that I had continued to put money into the market right through the 1969-70 bear market; the bad news was that I would have been far better off sticking with most (but not all) of my original holdings. Some lessons here.  Lesson 4: Avoid fads. Past performance of a stock is a rotten predictor of future results. If everyone is talking about hot stocks, like the conglomerates back then, like internet stocks in 2000, or like nano-technology today, you're too late. Lesson 5: Don't let a market slump change your long-term investment plan. Had I gotten discouraged and quit putting money in the market in 1970 (and then later in 1974-75) I would have missed out on the spectacular gains of the market rebound. Lesson 6: Don't check the price of a stock (or mutual fund) after you've sold it. After you've made a decision, stick with it. Look ahead, not behind; remember, today is the first day in the rest of your life. The "what-if game" (What if I bought this? What if I hadn't sold that?) only leads to recriminations and beating yourself up over something you can't do anything about. By late 1973, my portfolio was worth about $46,000, but I also had three young children who would eventually be heading off to college. And then came the 15-month grinding bear market of 1974, a new job with AT&T, and a move to New Jersey. All of which certainly did not lead to any spare change in my pockets. But remembering the spectacular recovery of just four years earlier led me to believe that it was worth some serious belt-tightening in order to continue to put some new money into the market. I had opened a college mutual fund for each of my three kids when they were about 7 years old and all of my new money went into these funds so my own portfolio didn't grow much. In fact I put some money from my portfolio into the kids' funds. However, by the time they were college age, there was enough in their funds to send each of them to college for four or five years. Lesson 7: Dollar-averaging (continuing to invest the same amount of money every month) really works. The mutual funds I signed on with for the kids required a fixed amount be put in every month (I don't think these type of funds are around anymore). By sticking with the program, and increasing the amount when I could, I met my goals and, in fact, was able to pay for five years of college for two of my kids who didn't finish up in four. Lesson 8: Don't panic. If there was ever a time in my life to panic, 1974 was it. Looking for a new job. Move to Morris County, one of the most expensive areas in the U.S. Stock market down 40%. Committed to starting a personal computing magazine in my spare time. Marriage shaky. My parents retire to Florida and want us to come and visit. Yikes!

In the late 70's, my life came almost totally unglued. The little personal computing magazine that I had started as a hobby in late '74 had 200,000 circulation, a staff of 20, and was growing like topsy. I had quit my job with AT&T and given up all the big-company benefits to work 16 hours a day at Creative Computing for no salary at all and, of course, no benefits. I was separated from my wife, living in a room adjoining my office, driving a car on its last legs, and pretty messed up. To make matters worse, for almost the next six years I virtually ignored my investments, made some very occasional buys and sells, put in practically no new money, and didn't even do any end-of year rebalancing.  I sold Creative Computing to a large publishing company in 1983, stayed on for three years as editor/publisher, and then left for new pastures in late 1985. It was then also that I took a close look at my stock portfolio and was dismayed with what I found. True, it had grown in value and was worth a little more than twice its value in 1973. That doesn't sound so bad until you consider that the Dow Jones had gone from about 800 to 2400 and the S&P 500 had done even better. So if I had just stuck my money in an index fund, I would have been far better off.

I sold Creative Computing to a large publishing company in 1983, stayed on for three years as editor/publisher, and then left for new pastures in late 1985. It was then also that I took a close look at my stock portfolio and was dismayed with what I found. True, it had grown in value and was worth a little more than twice its value in 1973. That doesn't sound so bad until you consider that the Dow Jones had gone from about 800 to 2400 and the S&P 500 had done even better. So if I had just stuck my money in an index fund, I would have been far better off.Moreover, some of the stocks in my portfolio had decayed into out-and-out dogs that should have been sold years earlier. My broker had made them sound wonderful in 1972, but they were stocks built on dreams and promises. I was so discouraged that I totally overreacted, sold almost everything, and put 80% of my money in municipal bonds for the next 8 years. Sure, I saved on taxes and it was a totally safe strategy, but I missed out on one of the best stock market runs of the last 30 years. What a dope! Sometimes, the lessons you learn are negative ones. This was one of those times. Lesson 9: Pay attention to what's going on with your investments. No stock is safe forever. Even the bluest blue chip can turn into a cow chip. The old maxim of "buy and hold forever" doesn't work very well in an economy as vibrant as exists in the world today. Lesson 10: Hold onto your winners and sell your losers. If you wouldn't buy more of a stock today on which you have a loss, sell it. Don't wait to "get even." Chances are there are better ways to invest your money. No well-managed store keeps obsolete goods in inventory; neither should you keep losers in your investment portfolio. Lesson 11: Take your losses quickly and your profits slowly. Every 50% loss begins with a 10% loss. Better to take the loss sooner, not later. Lesson 12: Stick to your plan. I was incredibly foolish to abandon my long-term plan because I had let small losses grow into big ones. The market is going to go up and down. Even if it's going up, you might not own the best performers, but if you are diversified and stick to your plan, in the long run you'll make out just fine.

During my career in computer magazine publishing, I travelled a great deal to Europe and the Far East. After one trip around the world I decided, almost on a whim, to make investments in ten high-quality foreign companies which I personally knew something about. These companies were in Japan, Hong Kong, Singapore, Germany, France, Sweden, and the UK. As it turned out, these investments did very well and three of them are still in my portfolio.

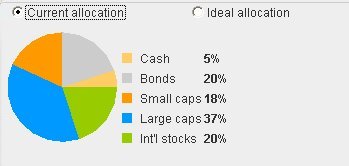

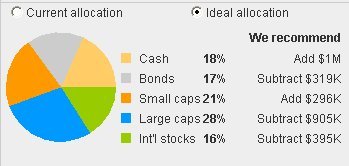

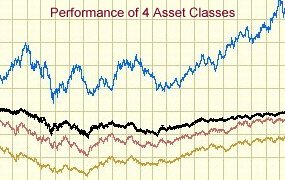

During my career in computer magazine publishing, I travelled a great deal to Europe and the Far East. After one trip around the world I decided, almost on a whim, to make investments in ten high-quality foreign companies which I personally knew something about. These companies were in Japan, Hong Kong, Singapore, Germany, France, Sweden, and the UK. As it turned out, these investments did very well and three of them are still in my portfolio.I gradually started getting back on track in the early 90's. My father died in 1992, my mother's health started going downhill, and I was left to pay her bills and manage her finances. Obviously, the needs of an older person living on Social Security plus the income from an investment portfolio are far different from a 22-year-old getting out of school or someone in the middle of a work career. In her case, bonds, Treasury notes, and preferred stocks made a lot of sense, so I set out to learn as much as I could about fixed income investments. One thing led to another, and I read practically every book and article on investing written in the past 50 years. I subscribed to eight investment newsletters and totally immersed myself in the field. While I had learned a lot of lessons on my own, I learned a great deal more from reports of academic studies, from the writings of great investment gurus like Ben Graham and John Templeton, and from newsletter editors like Marty Zweig and Dan Sullivan. As a result of all this, I refined my plan, concentrating more heavily on the right allocation of assets to fit my investment goals, my stage in life, and my tolerance for risk. I diversified still further into bonds (muni, corporate, and foreign), stocks (doemstic and foreign), real estate (mostly in the form of REITs), natural resources (gold, gas, timber), and, of course, cash.  Lesson 1 (Repeated): Diversify! Your asset mix should include not just several stocks, but large and small cap stocks, growth and value stocks, and foreign stocks along with a mix of bonds, short-term investments, real estate, commodities, and perhaps even other things.

Lesson 1 (Repeated): Diversify! Your asset mix should include not just several stocks, but large and small cap stocks, growth and value stocks, and foreign stocks along with a mix of bonds, short-term investments, real estate, commodities, and perhaps even other things.Lesson 13: Be realistic about your tolerance for risk. Ask yourself, "How well will I sleep if my investments drop in value by 10%? By 20%? By 50%?" If a big dip is going to get to you, as it did to me, you need to put a higher proportion of your portfolio in bonds, in utilities, in "value" stocks, and even in cash. Lesson 14: Get the best investment advice you can--and then think for yourself. Now I'm not saying not to buy a stock recommended by a stock broker or a magazine article or a tip from a friend, but don't do so blindly. Do some research on your own. There are scores of web sites with good, solid research data. Use them.

You might notice that for the most part I continued to add money to my investments through good times and bad. Over a 50-year period, there were only four times when I sold stocks or bonds to buy something else: once, when I got out of the Army to put a down payment on a house, once for the initial funding of my kids' college mutual funds, once to start my magazine publishing business, and most recently, to buy a new car. But these are the reasons that you put money in the market in the first place. Lesson 15: Avoid spending the principal. Set some money aside in a savings or money market account for smaller expenses like furniture, vacations, hobbies, computers, car repairs, and babies. And don't forget to reinvest the interest and dividends from your stocks and bonds. Mutual funds make this easy becasue reinvestment is automatic; with individual stocks and bonds you'll have to do it yourself. Make a mental note to yourself that when your monthly statement shows a cash balance of more than, say, $1000, to buy some more shares of one of your holdings. Lesson 16: In investing, you're not going to be right every time. You're not going to always be able to buy low and sell high. But remember, the object is not to be right all the time but to make money when you are right. That means sticking to your plan, investing in good-quality, profitable companies, putting money into the market on a regular basis, selling losers sooner rather than later, and sticking with your winners. | ||||||||||

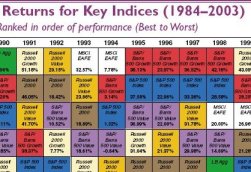

| In case you missed them, there are two pages of deeper discussion of the items above: Diversification of Asset Clsses Foreign Stocks Can Improve Return and Decrease Risk Click here for a page of practical tips on managing your money. Click here for links to the best investment sites on the web. | ||||||||||

| ||||||||||

| © 2021. Web site design by Dave Ahl, e-mail swapmeetdave@aol.com | ||||||||||